Legislature Looks at Reducing Business Tax

Governor Greg Gianforte, Senator Josh Kassmier, R-Fort Benton, and local ag producers are urging support for reforms to the business…

.

Governor Greg Gianforte, Senator Josh Kassmier, R-Fort Benton, and local ag producers are urging support for reforms to the business…

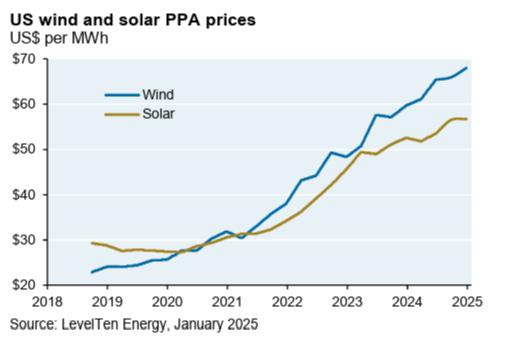

Energy prices are rising due to US tariffs on Chinese solar panels, a tripling of insurance premiums in MISO, ERCOT,…

Confidence among American consumers fell sharply in February, hitting a 29-month low, while long-run inflation expectations recorded their biggest monthly…

Commercial Chase Moore, 50 Moore Ln, Com Footing/Foundation, $450,000 Winchell Real Estate Holdings|Scott Roby Remodel, 1807 Grand Ave, Com Remodel,…

The Montana Aeronautics Board has allocated more than $3.2 million in funding for fiscal year (FY) 2026. This funding is…

By Sarah Roderick-Fitch, The Center Square A coalition of state attorneys general is filing an amicus brief in the U.S.…

Marking the 250th anniversary of Patrick Henry’s famous speech. By Lawrence W. Reed, Foundation for Economic Freedom In St. John’s…

Early this week, Coca-Cola Bottling Co. High Country in partnership with Dick Anderson Construction held a gathering at which the…

By Roger Koopman At an early age, we taught our kids to learn from others and to think for themselves. …

Roger Pielke Jr., from substack.com An important new paper published this week in Nature Communications looks at the historical record…